Master of Science Accounting

Build the advanced accounting and analytics skills needed in today’s accounting profession—in just seven months with CPA-aligned coursework.

Program details

-

Commitment

Full-time, 7 months

-

Entry Terms

Summer

-

Visa Compliant

Yes

-

STEM-designated

No

-

Program Options

Yes

-

Locations

Boston

This program is ideal for

Accounting majors looking to level up before pursuing CPA licensure

Aspiring auditors or tax accountants seeking specialized expertise

Future MBA students looking to stack credits toward a D'Amore-McKim MBA

Application deadlines

*Final deadline for international applicants needing a new F-1 or J-1 visa

An accelerated path to a high-demand accounting career

- Complete your master's in just seven months.

- Designed for undergraduate accounting majors.

- Build advanced accounting expertise and in-demand analytics skills.

- Choose a focused track in Audit or Tax to match your career goals.

- Learn from a curriculum shaped by top firms to meet evolving industry needs.

Program options

An accelerated master's designed for accounting majors

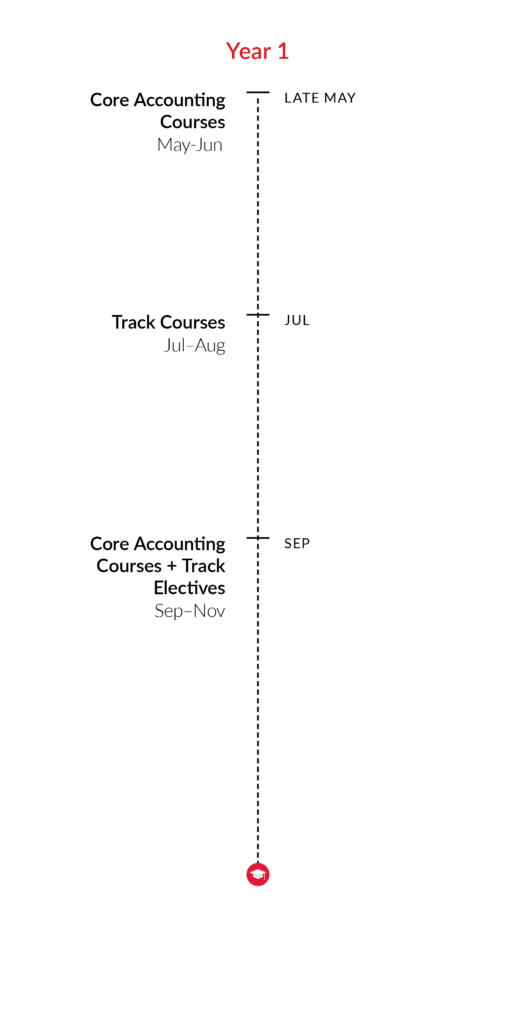

Earn your master's in Accounting, and the 150 credits required to sit for the CPA exam, in just seven months. Designed for students with a U.S. undergraduate degree in accounting, this intensive program builds advanced expertise in accounting and analytics while offering two tracks, Audit or Tax, to align your studies with your career goals. You'll graduate ready to launch your career during the industry's busy season.

Locations

Student voices

Dive deeper

Faculty & learning

Our world-class faculty bring years of experience, innovative leadership, and global perspectives to their teaching and are dedicated to preparing you for success in a rapidly evolving business world. You'll learn from professors of practice with deep experience at Big 4 and top accounting firms, as well as from the nation's leading behavioral accounting research group.

Professional licensure

Earning your MS in Accounting is a critical step toward CPA licensure and a career in public accounting. Many students begin taking sections of the licensure exam during their final term; ensuring they're well-positioned professionally to graduate in December during accounting's busy season. For information on where this program will help you achieve professional licensure, please visit Northeastern's consumer information website and review Professional Licensure Disclosure.

Careers & support

You'll receive personalized career support from the Graduate School of Professional Accounting's student services team. They'll work with you one-on-one on professional goals and connect you with the right opportunities through their strong employer relationships. Through networking events and learning opportunities, you'll continue to grow professionally—both in and out of the classroom.

Alumni network

One of the most valuable benefits of earning your master's degree from D'Amore-McKim is the chance to become part of our elite alumni network—more than 62,800 members strong across 154 countries—who regularly connect through events, programs, services, chapters, volunteering, and more. As a graduate of the Graduate School of Professional Accounting, you'll also join a close-knit, 4,000+ member alumni community known for mentoring students and opening doors at top accounting firms.

International students

Northeastern's Office of Global Services provides the expertise and support you need to maintain compliance through your immigration, academic journey, and employment experiences—including any Curricular Practical Training deemed necessary or integral to your academic program and Pre-Completion and Post-Completion Optional Practical Training work authorization.

Applicant FAQs

upcoming addmissions events

Graduate Accounting Programs “Ask Me Anything”

Request more information

Whether you're ready to apply or just exploring, fill out this short questionnaire to join our contact list and receive timelines, updates, and event invitations.